A key factor for what will happen with the future world economy is how fast will Chinas economy grow over the next twenty years. In 2010, the Asian Development Bank projected that China might grow at a 5.5 percent average during the two decades to 2030, and if it improves education, research, and property rights, that might climb to 6 percent. A 31 page research paper by Economic historian and Nobel laureate makes a detailed case for how China can achieve 8% per year GDP growth from 2000 to 2030.

Business Week cited and referenced the Fogel paper in a recent article. They indicate there are still strong reasons to believe fast growth remains possible for China during the next two decades. Fogel’s 31 page paper was written in 2006.

From Business Week –

Economic historian and Nobel laureate Robert Fogel argues there is certainly the potential for China to continue growing at 8 percent until 2030. Despite an aging (PDF) population, there are still opportunities for more adults to work. And more of that labor will likely move into more productive sectors over time—out of agriculture and into manufacturing and services. These two factors alone could account for 30 percent of the country’s continued growth, Fogel suggests.

From the Fogel paper –

Since about 30 percent of China’s growth rate is likely to continue to come from the interindustry shifts (agriculture to manufacturing and services) and modest increases in the labor force participation rate growth rates of labor productivity within sectors need only average about 5 percent per year.

Several factors suggest that such growth rates are likely. Despite the remarkable advances of recent decades, the average technology is still well below best prevailing practice in each of the three sectors. Hence, growth in each sector will be stimulated by the diffusion of the best prevailing practice. Moreover, the frontier of technology is moving out rapidly, especially in the industrial and service sectors, but also in agriculture. Third, the investment in capital, especially human capital, is capable of rapid improvement in the next several decades. Finally, despite the preoccupation with possible overstatement of the Chinese growth rate due to inflated estimates of growth sent from localities, on balance it is likely that the true Chinese growth rate is understated, especially in the service sector, due to the failure adequately to account for improvements in the quality of output and the underreporting of small firms. I now want to elaborate briefly on these last two factors and assess their likely impact on growth rates over the next two or three decades.

In 2002, the Chinese Communist Party announced a goal of quadrupling per capita income by the year 2020. Starting at income levels of the year 2000, this would require a growth rate of 7.2 percent per annum in per capita income or close to 8.0 percent in GDP. Such unresolved and emerging problems as growing income disparities, increasing pollution, pressures on infrastructure, the inefficiency of state owned enterprises, and political instability are often cited as reasons to doubt the attainability of the CCP’s goal. However, China’s progress in addressing fundamental constraints that might limit rapid economic growth augurs well for the success of its economic goals. Although there are disagreements about economic policy among top leaders, the continued transformation into a market economy and the promotion of increasing local autonomy in economic matters are not in doubt. In education, China has substantially increased the percentage of its workforce receiving a college education, and continuing growth in this investment in human capital could account for a large portion of the desired growth rate. In addition, the value of improvements in the quality of economic output unmeasured by GDP, such as advances in the quality of health care and education, could raise reported growth rates by as much as 60 percent. Finally, the government’s increasing sensitivity to public opinion and issues of inequality and corruption, combined with improving living conditions, have resulted in a level of popular confidence in the government that makes political instability unlikely.

Education and Productivity

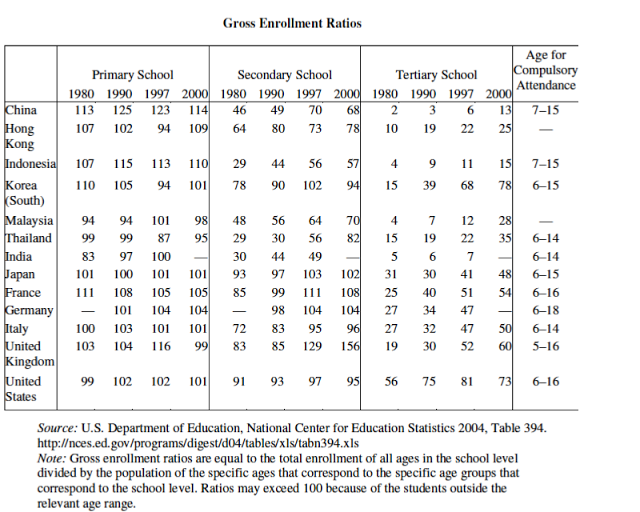

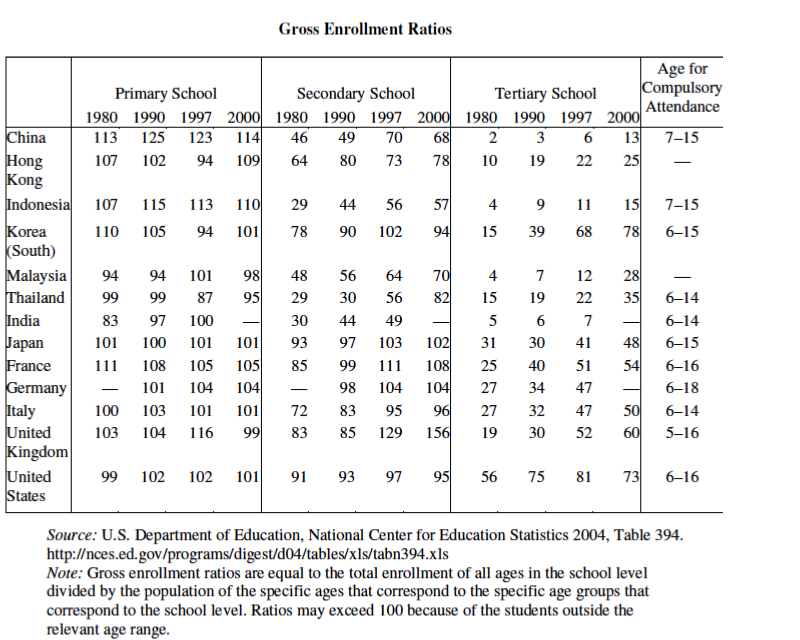

In the USA a college educated worker is 3.1 times as productive (per capita income), and a high school graduate is 1.8 times as productive, as a worker with less than a ninth-grade education. The bottom half of the table indicates the contribution of various scenarios of increases in enrollment ratios. Labor enhancement would grow at the rate of 1.8 percent per annum if the secondary ratio reached one hundred in 20 years. Multiplying this figure by the labor share indicates that such an achievement would add about 1.1 percent to the growth rate of labor productivity.

Labor enhancement would grow at 7.4 percent per annum if the tertiary ratio rose from 6

to 25 in the next twenty years, which would put the tertiary level of education in China at about where the Western European nations were in 1980. That level of labor augmentation would add 4.4 percent to the growth rate of labor productivity, and by itself would account for over 60 percent of the target set in 2002. With a more ambitious expansion of higher education, reaching enrollment ratios of 50 in 20 years, labor augmentation would grow at 11.2 percent. The rate of investment in human capital would by itself add 6.7 percent to the overall growth rate.These targets for higher education are not out of reach. It should be remembered that as recently as 1980, the Western European nations had ratios of about 25. Only the United States was above 50. The movement to enrollment ratios of 50 in Western Europe was a product of the last two decades of the twentieth century. In the case of the U.K., two-thirds of the increase from 19 to 52 percent took place between 1990 and 1997.

Errors in the Measurement of Output and the Value of Improved Health

So far I [Robert Fogel] have focused mainly on factor enhancement to support my contention that China is likely to achieve its growth targets. I [Robert Fogel] want to turn now to the problems of measurement on the output side of equation. Errors in the measurement of national income from the output side have become increasingly severe. It is now clear that official estimates of GDP for the United States badly underestimate U.S. economic growth because they do not take into account improvements in the quality of output, especially in such services as education and health care. Children in secondary schools are taught more about science and technology today than postgraduate college students used to be taught a generation ago, let alone two generations ago.

Even more dramatic are the improvements in health care. A century and a half ago,

people in their late thirties and early forties were more afflicted by chronic disabilities people in their late sixties and early seventies are today.Yet most of these great advances in health care and education are overlooked in the GDP

accounts, because the values of these sectors are measured by inputs instead of by output. An hour of a doctor’s time is considered no more effective today than an hour of a doctor’s time was half a century ago, before the age of antibiotics and modern surgery. It has recently been estimated that the value of improvements in health care, if properly measured, are at least twice the cost of health care, but such calculations have not yet made their way into the GDP accounts (Cutler and McClellan 2001; Murphy and Topel 2003; Nordhaus 2003). In the case of the United States, my [Robert Fogel] own rough estimates indicate that allowing for such factors as the increase in leisure time, the improvement in the quality of health care, and the improvements in the quality of education would come close to doubling the U.S. annual growth rate of per capita income over the past century (from 2.0 to 3.6 percent per annum).Studies of the value of a statistical life year in rich and poor nations suggest that the value of an additional year of life in China is about 3.5 times per capita income (see, e.g., Murphy and Topel 2002; Viscusi and Aldy 2003). Hence, the value of the unmeasured improvements in life expectancy may have been high enough to raise the rate of economic growth between 1980 and 2000 by about 60 percent. If the true growth of GDP between 2000 and 2040 is 13 percent instead of 8 percent, then the true size of the Chinese economy in 2040 will be about 6 times the size of the measured economy. Of course, if both the United States and China similarly neglect changes of quality in their measurements, the relative ranking of the two economies may not be changed significantly

Urbanization and a college education workforce overlap

Nextbigfuture covered a Goldman Sachs report on Hukou reform and urbanization in China.

China is also going to get several hundred billions more from marine economy.

All local governments in China’s eastern and coastal regions, except Shanghai, have unveiled investment plans to develop marine-related projects such as fishing, marine tourism services, shipping and offshore oil and gas exploration to stabilize local economies.

Local governments hope the so-called “marine economy” will contribute to a combined gross domestic product (GDP) of 7.05 trillion yuan (1.11 trillion U.S. dollars) by 2015, a goal much higher than the 4.55 trillion yuan seen in the marine economy last year.

China’s inland areas appear able to absorb more investment to carry on the investment model and provide the overall economy with more GDP growth. The eastern coastal areas will have more of a shift to consumer consumption. There is consumer consumption increases in the inland areas as well.

Michael Pettis Argues the Bearish View

I [Michael Pettis] think the current consensus of 5-7% average growth for the next ten years is still too high, and the historical precedents make it clear that we tend to underestimate sharply the cost of an adjustment of this nature (think for example of the USSR in the early the 1960s, Brazil in the late 1970s or Japan in the late 1980s, all of whom suffered far more difficult subsequent adjustments than even the sceptics had expected). Already this year Beijing has announced growth rates for China of 7-8%, but a large number of economists in China, based on alternative measures of economic activity, doubt the accuracy of the official numbers, with some arguing that real growth this year may be as low as half the posted rates.

I [Michael Pettis] am not smart enough to say if they are right or wrong, but one way or the other I expect growth forecasts among China bulls to continue declining over the next few years. If, as I expect, Beijing seriously begins to rebalance its economy in 2013, I believe as I always have that the average annual growth rate over the following ten years will not exceed 3-4%.

Michael Pettis believes rebalancing has started

Nextbigfuture still sees 8.0 to 8.5% growth to 2020 and 7.0% from 2020-2030

My predictions of China’s growth rate have not changed much over the last 7 years. I still see strong economic growth. Any slower changes in nominal GDP growth will be from lower inflation and slower appreciation of the currency.

Year GDP(yuan) GDP growth USD/CNY China GDP China+HK US GDP 2011 47.2 9.2 6.3 7.5 7.8 15.2 2012 53 8.0 6.1 8.7 9.0 15.9 2013 59 8.5 5.8 10.2 10.5 16.5 2014 66 8.5 5.5 11.9 12.2 17.2 2015 73 8.5 5.2 14 14.3 18 2016 80 8 4.9 16.3 16.7 18.8 2017 88 8 4.6 19.1 19.5 19.6 2018 97 8 4.3 22.6 23 20.5 2019 107 8 4.1 26 26.5 21.5 2020 115 7.5 3.9 29.6 30 22.4 2021 125 7.5 3.7 33.7 34.2 23.4 2022 135 7.5 3.5 38.5 39 24.5 2023 145 7 3.3 44 44.5 25.6 2024 157 7 3.1 50.6 51 26.7 2025 170 7 3 56.5 57 27.9 2026 183 7 3 61 61.5 29.2 2027 198 7 3 66 66.4 30.5 2028 214 7 3 71.2 72 31.9 2029 235 7 3 78.4 79 33.3 2030 259 7 3 86.4 87 34.8

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.