In the Diplomat, Minxin Pei (professor of government) tries to raise an alarm about the debt levels at China’s banks and local government. This has been an issue that has been discussed for at least two years.

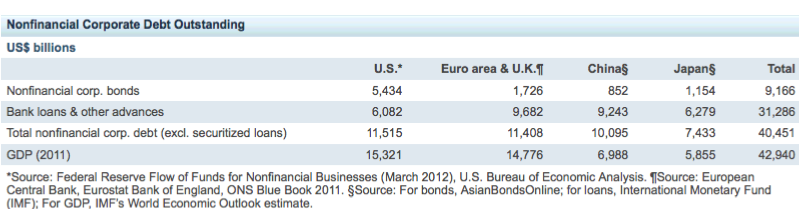

The global “wall” of nonfinancial corporate debt maturities coming due from 2012 to 2016 is not new to market observers. Less discussed is the incremental financing that corporate debt issuers will need over this period to fund capital expenditure and working capital growth. Standard & Poor’s Ratings Services estimates the total amount of refinancing and new money requirements over the next five years at between $43 trillion and $46 trillion. This demand for funds will potentially compound the credit rationing that may occur as banks seek to restructure their balance sheets, and bond and equity investors reassess their risk-return thresholds. These factors, amid the current eurozone crisis, a soft U.S. economic recovery following the Great Recession, and the prospect of slowing Chinese growth, raise the downside risk of a perfect storm for credit markets, in our view.

Our assumption is that there is sufficient capital market and bank lending capacity to absorb the majority of the $30 trillion that we estimate nonfinancial corporate borrowers will need to refinance over the next five years in the U.S., euro area, the U.K., China, and Japan. However, the $13 trillion to $16 trillion required to fund future growth could be more at risk. Given our expectation that certain borrowers may find the availability of bank financing more limited than in the past–and when available, at a higher cost with likely more onerous terms and conditions–alternative providers of debt financing may be set for a new challenge.

If China kicks the debt issue down the road into 2017, then China’s nominal GDP is $14 to 18 trillion. The current debts could have grown by 20% at that point.

Europe, Japan and the United States with slow growth are unable to noticeably grow faster than the debt interest.

Deferring the “debt bomb” will work for China. The debts of Greece, Spain, and Italy do not work out that way.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.