McKinsey has an analysis of the Chinese consumer in 2020

Many of the changes taking place in China are common features of rapid industrialization: rising incomes, urban living, better education, postponed life stages, and greater mobility. Japan saw similar changes in the 1950s and 1960s, as did South Korea and Taiwan in the 1980s.

But some unique factors are also at work, such as the government’s one-child policy and the marked economic imbalances among regions. Our analysis reveals important insights into the likely demographic and socio-demographic profiles of Chinese consumers at the end of this decade.

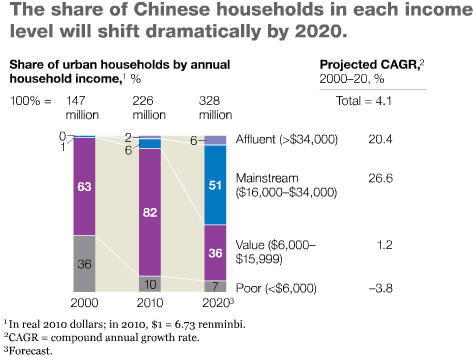

Changes in economic profiles have been and will continue to be the most important trend shaping the consumer landscape. The Chinese are certainly getting richer fast: the per-household disposable income of urban consumers will double between 2010 and 2020, from about $4,000 to about $8,000. That will be close to South Korea’s current standard of living but still a long way from its level in some developed countries, such as the United States (about $35,000) and Japan (about $26,000).

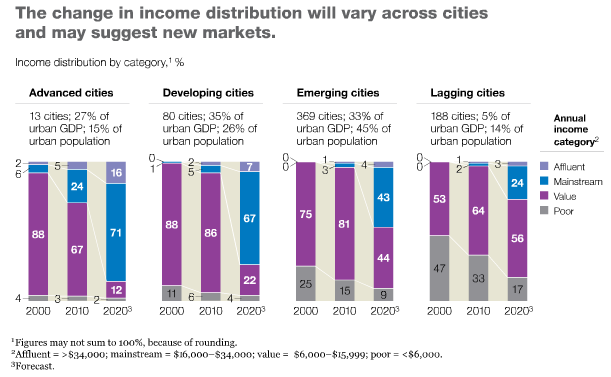

Our consumption model suggests that in 2010, average household spending for value, mainstream, and affluent consumers was about $2,000, $4,000, and $12,000, respectively. These figures will jump to $3,000, $6,000, and $21,000, respectively, by 2020. So although all consumers will increase their spending, the gaps between different income groups will widen significantly. Stark disparities in standards of living are emerging in China.

Annual volume growth rates of more than 20 percent are foreseeable for luxury SUV cars, compared with around 10 percent for basic family models. China had already become a leading luxury market by 2010 and could overtake Japan to become the biggest such market by 2015.

Research undertaken by McKinsey suggests that, barring major world economic shocks, China’s GDP will indeed continue to grow, at an annual rate of some 7.9 percent over the next ten years compared with 2.8 percent in the United States and 1.7 percent in Germany. The difference henceforth is that consumption, rather than investment, will be the driving force. It will account for 43 percent of total GDP growth by 2020, compared with a forecast contribution from investment of 38 percent.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.