Dan Yurman discusses China’s ambitious nuclear energy program

Dan discusses the issues around scaling the workforce, supply chain and uranium.

I will review the scale of the build and the scaling up of world Uranium supply. The increase in nuclear construction is mostly not happening in Europe or the United States. Europe and the US have nearly flat energy generation growth because of slow growing economies.

I also had written an article about China’s nuclear build and the exporting of cheap reactors and how that could solidify the high end projections of the WNA for 2030.

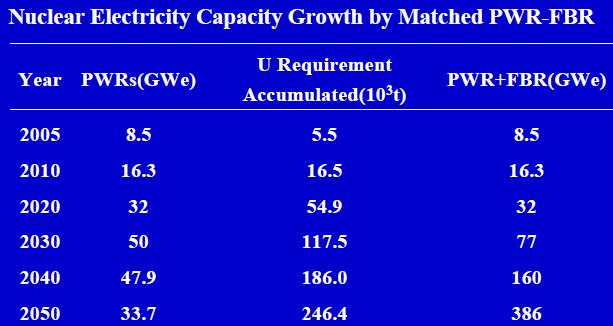

114GWe may be 7% of the 1600GWe that China should have in 2020 but China is forecast about 6500TWH (terawatt hours) for 2020 and 114 GWe would be about 800 TWH or about 12% of generation.

Cameco (Canada is targeting doubling uranium to 20,000 tons/yr by 2018

Other suppliers and resources in Canada for another 10,000 tons/yr

Kazakhstan can go to 40,000 tons/yr

Namibia can go to 30,000 tons/yr

Niger can go to 15,000 tons/yr

Australia could go to 30,000 tons/yr

Other countries 50,000 tons/yr

Tailings can be re-enriched for another 10,000 tons/yr

This would be over 200,000 tons/year of conventional uranium supplies.

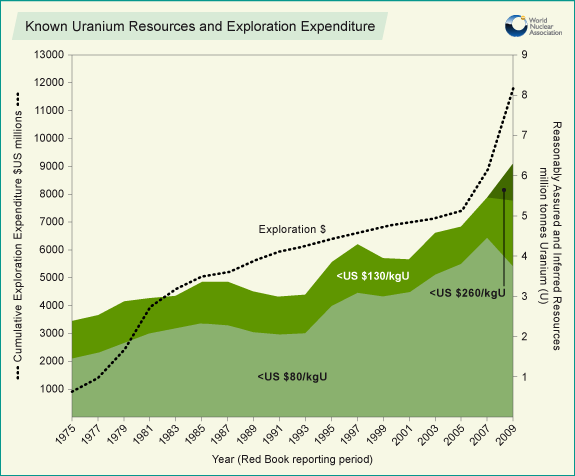

If there is over 100 billion per year being spent on nuclear plant construction then Uranium exploration will increase from the $1 to 1.5 billion/year level of recent years.

Up until 2009, there had only been $8 billion spent on uranium exploration.

The balance of plants for a coal power plant is very similar to nuclear. Why would nuclear costs for construction go up so much when coal plants did not. We will see what happens with costs.

Namibia targets 26,000 tons of uranium per year by 2015

8000-9000 tons per year expected from one mine in Niger. Imouren (2013 at 6000 tons and then 8000-9000 tons in 2018)

China plans for longer term uranium supply includes more uranium from phosphate if regular supplies are not sufficient and then to transition to a closed cycle with breeders and off site reprocessing.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Featured articles

Ocean Floor Gold and Copper

Ocean Floor Mining Company

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.